Caroline Duncan

Caroline Duncan

9 min read

How to Notify Employees During a Cyberattack (When Email & Systems Are Down)

When a cyberattack hits, the channels you’d normally use to warn employees — email, Teams, the intranet — are often the first casualties. They may be...

The cybersecurity landscape is always shifting, with threats becoming more sophisticated all the time. In the banking and financial sector, the stakes are high: not only are large amounts of money at stake, but when banks and other financial systems are compromised, the disruption to the economy as a whole can be significant.

A key priority for banks should be raising awareness of cybersecurity issues among employees and making the most of innovative communication tools, such as DeskAlerts, to cut through the digital noise and ensure that important information on cybersecurity topics is being received.

Table of contents

The Importance of Being Aware of Cybersecurity Trends

The Top Cybersecurity Threats for Banks

Examples of cybersecurity attacks in banks

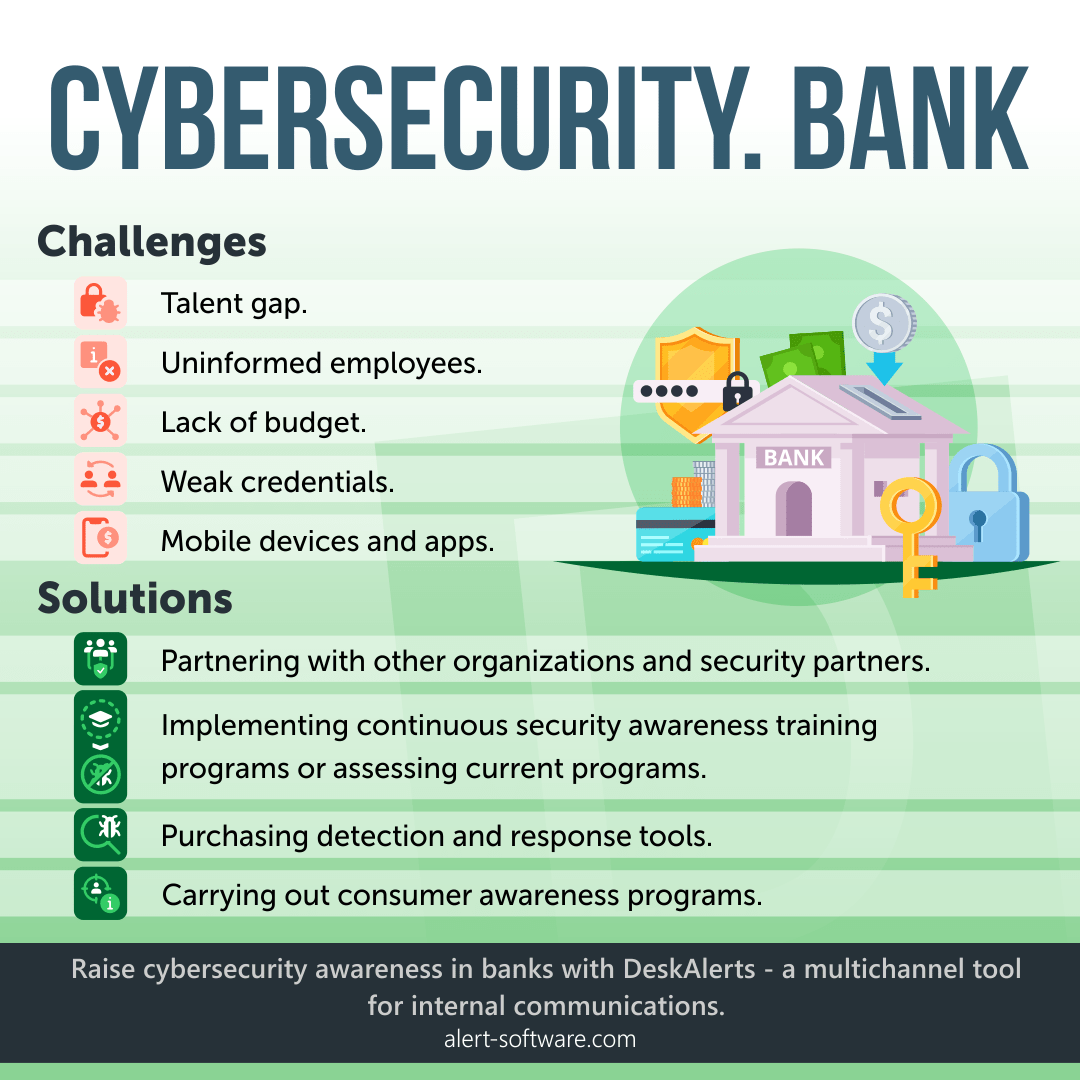

Cybersecurity challenges banks face

Solutions to cybersecurity challenges in banking

According to Sophos's 2025 State of Ransomware report, financial services organizations ranked among the hardest-hit sectors (alongside healthcare and manufacturing). Also, two-thirds of financial services respondents attributed their vulnerability to inadequate protection or undetected security gaps, pointing to the growing sophistication of attacks rather than a lack of awareness.

The main reasons to be vigilant around cybersecurity trends include:

Staying informed about the risks of cybersecurity has been an important regulatory requirement for financial institutions in the United States, with new reforms coming into place in recent years.. Banks are now required to inform the federal regulator about any incidents that have occurred that can affect the viability of their operations or their ability to deliver services and products.

They're also required to report anything that may potentially occur and anything that could affect the USA's financial sector's stability. These types of events include banking cybersecurity risks such as hacking, ransomware, and distributed denial of service (DDoS) attacks.

Similar rules are now in force across other major markets: the EU's Digital Operational Resilience Act (DORA) has applied to all financial entities across all 27 member states since January 2025; the UK's FCA and PRA operational resilience framework has been in effect since 2022; and Australia's APRA Prudential Standard CPS 230 came into force in July 2025.

According to a 2024 survey by the American Bankers Association, three out of four banks increased their technology budgets in fiscal year 2024, with cybersecurity cited as the primary area of investment — and no bank reported cutting its IT budget.

These are the top cybersecurity threats that are predicted to continue to cause grief for banks and financial institutions over the course of 2026.

Ransomware has been a major headache for organizations around the world for several years now, and doesn’t look like it's stopping any time soon. This is a method of cybercrime where files are encrypted, and users are locked out, with the criminals demanding money to re-access the system.

Organizations affected by ransomware attacks can find their systems crippled for extended periods of time, particularly if they don’t have backups. Paying ransoms to these criminals is also not guaranteed to result in your system's access being restored.

Remote and hybrid work are now permanent fixtures in the financial sector. According to Gallup, as of early 2025, nearly 80% of employees whose roles can be done remotely are working either hybrid or fully remote. And only 30% of companies plan to eliminate remote work entirely.

This sustained shift means financial institutions carry a larger and more distributed attack surface than ever before. Employees regularly access sensitive data and systems from home networks, personal devices, and unsecured connections that fall outside corporate IT controls, making extra vigilance not a temporary measure, but an ongoing operational requirement.

As more software systems and data are stored in the cloud, cybercriminals have seized upon this, and as a result, an increase in cloud-based attacks has been one of the most prevalent cyber threats to the banking industry.

Banks need to ensure that the cloud infrastructure is configured securely to protect from harmful breaches.

One of the biggest recent cyber threats to banking and finance is social engineering. People are often the most vulnerable link in the security chain – they can be tricked into giving over sensitive details and credentials. This can equally affect a bank’s employees or its customers.

Social engineering takes many forms; it might be through phishing or whaling attacks, or it could be by sending bogus invoices that purport to be from a trusted source. It’s important to keep your employees informed about social engineering tactics and how these threats continue to evolve.

Increase Message Visibility and Prevent Cybersecurity Breaches. Download for free

An increasingly popular method of malware distribution by cybercriminals is to target a software vendor and then deliver malicious code to customers and others in the supply chain in the form of products or updates that, on the surface, appear to be legitimate. These attacks compromise the distribution systems and enable the cybercriminals to enter the supplier’s customers’ networks.

Cyberattacks on banks and financial institutions have been a persistent threat. Some notable examples include:

Trying to implement cybersecurity mitigation strategies in the banking sector can be challenging. Some of the major cybersecurity challenges that banks need to overcome include:

Of course, there are still steps that banks and financial institutions can take to ensure that their systems are protected against common challenges to cybersecurity in financial services. This includes:

Communication is critical in banks and other financial institutions when it comes to raising awareness of cybersecurity in banking and preventing financial cybersecurity incidents.

Devise appropriate internal communications strategies on a range of cybersecurity topics to keep employees informed about their obligations to keep data safe, report breaches, be aware of new threats, and ensure that you have the appropriate tools and resources to deliver the information in a compelling and engaging way.

Increase Message Visibility and Prevent Cybersecurity Breaches. Download for free

Some of the ways banks can achieve this are through internal financial communications, including:

By planning ahead now to deal with potential cybersecurity threats and staying up to date with trends in cybersecurity, you can get on the front foot with cybersecurity in 6. There are always going to be new challenges to face with cybersecurity for banks, but if you have the right foundations, you’ll be well-prepared to tackle any emerging cybersecurity threats in the future.

The five biggest threats to bank security in 2026 are:

The biggest cybersecurity threat is human error. It is people who ultimately put data and systems at risk, either because they have been tricked into providing sensitive details, haven’t properly protected their passwords, have used weak credentials, have clicked on malicious links, or have opened suspicious email attachments.

Cybersecurity in banking is concerned with protecting the customer and their assets, as well as the bank’s resources and bottom line. Cybersecurity incidents can be extremely costly, time-consuming, and lead to regulatory fines or other legal action by aggrieved customers.

There are several proactive steps that can be taken to improve cybersecurity for banking. Types of security in banking often include:

Banks need cybersecurity to ensure that their customers’ data and money are safe from criminals. When there are data breaches, not only can customers come to harm, but the bank itself can suffer from irreparable reputational damage and may face legal costs and regulatory penalties as well.

Banks can ensure security by implementing various enhanced security measures, including requiring stronger login details, encrypting data, rigorous steps in account management, and implementing two-factor authorization.

Top cyber security risks in 2026 continue to be ransomware attacks, social engineering attacks, cloud security breaches, and vulnerabilities with Internet of Things (IoT) systems.

One of the biggest cybersecurity threats to the banking industry is a Distributed Denial of Service (DDoS) attack, which involves overwhelming a bank's online systems with traffic from multiple sources, effectively making it unavailable to customers. This type of attack can be carried out by a large botnet or a group of hackers and can result in significant financial losses for the bank, as well as a loss of customer trust and damage to the bank's reputation.

There are several potential cyberattacks that banks can face. These include:

Technology risk for banks refers to the potential negative impact that technology-related issues can have on the operations, security, and reputation of a bank. This includes cybersecurity risk, IT systems failures, third-party risk, regulatory risk, and innovation risk.

In 2026, the threat landscape for cybersecurity continues to evolve, with several prominent concerns. Advanced persistent threats (APTs) remain a significant menace, leveraging sophisticated techniques to infiltrate networks and exfiltrate sensitive data. Additionally, ransomware attacks persist, targeting individuals, businesses, and even critical infrastructure, causing widespread disruption and financial loss. The proliferation of Internet of Things (IoT) devices introduces new vulnerabilities, amplifying the potential for large-scale breaches and botnet attacks. Other current cybersecurity threats are from emerging cybersecurity technologies such as artificial intelligence and quantum computing, which potentially enable more potent cyber-attacks and are likely to also be a focus for the future of cybersecurity.

In 2026, cybercrime is predicted to escalate, fueled by increasingly sophisticated tactics and the widespread adoption of emerging cybersecurity technologies. Ransomware attacks are expected to become even more prevalent, targeting a broader range of organizations and industries.

The exploitation of IoT vulnerabilities may lead to more extensive botnet-driven assaults. As cybercriminals adapt to evolving security measures, collaboration between public and private sectors becomes crucial in combating these threats effectively.

One of the most common and persistent cybersecurity threats is phishing. Phishing involves tricking individuals into divulging sensitive information such as passwords, credit card numbers, or personal details by posing as a trustworthy entity in electronic communication. It's often carried out via email, but can also occur through text messages, social media, or other communication channels. Phishing attacks continue to evolve in sophistication, making them a significant concern for individuals and organizations alike.

Ransomware stands as one of the biggest cybersecurity threats to businesses. It encrypts data, demanding payment for decryption, causing significant financial losses and operational disruptions, often exploiting vulnerabilities in networks and systems.

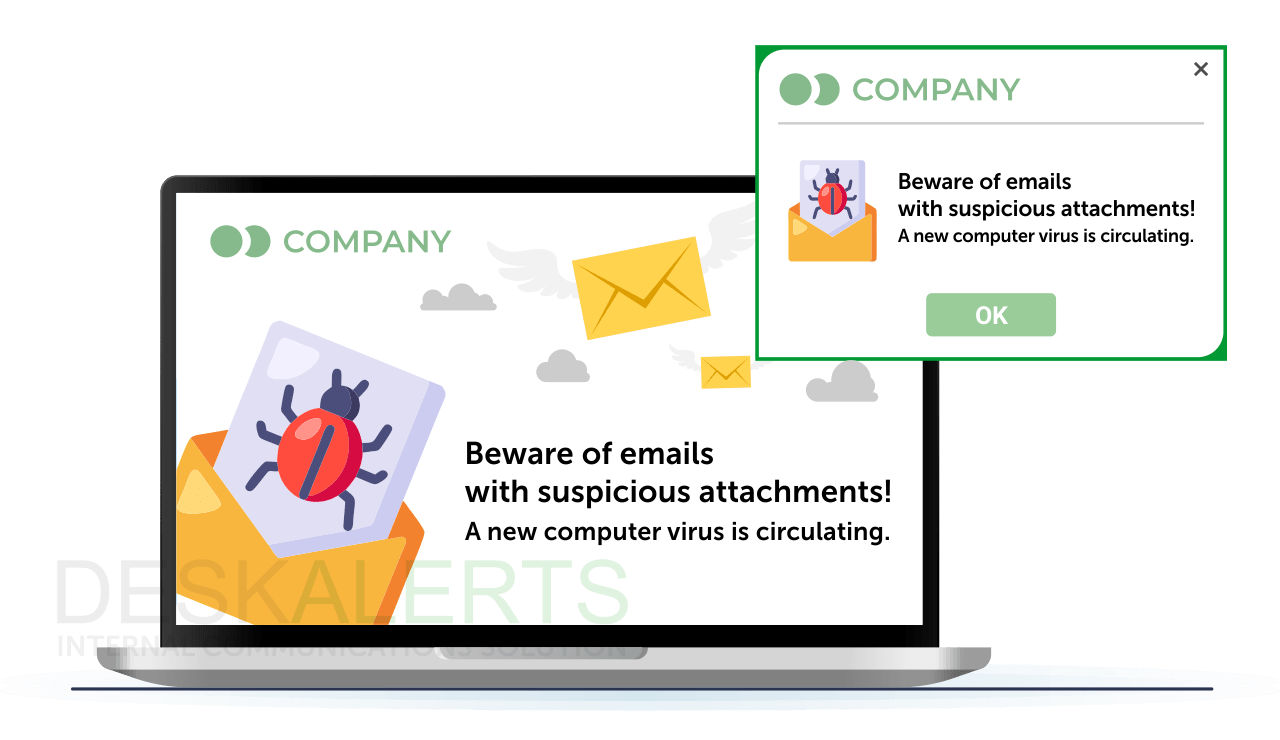

Send urgent notifications to PCs, phones, tablets, digital signage, and other corporate devices.

Display high-visibility alerts directly on employees' screens to help ensure critical messages are seen and acknowledged. Reach employees even when computers are locked, in screensaver mode, or idle.

9 min read

When a cyberattack hits, the channels you’d normally use to warn employees — email, Teams, the intranet — are often the first casualties. They may be...

6 min read

Communication failures rarely happen because someone “forgot to send an email”, but rather because channels like email, Teams, Slack, and SMS were...

16 min read

Teams is down. Tickets to the help desk flood in faster than anyone in the IT team can triage. Email is useless because half the staff can't sign...

4 min read

Sending employees a cybersecurity awareness email or newsletter is one of the best ways to keep security front of mind in your organization. Using...

7 min read

In today's rapidly evolving financial landscape, banks must stay ahead of industry changes, regulatory updates, and technological advancements....

9 min read

Last year was a record-breaking one in terms of the amount of data that was lost around the world in breaches and cyberattacks. It also set a new...